Here, we are making an effort to clear the basic concept of Marginal Costing. The most important factor which distinguishes marginal costing from all other types of costing is that in marginal costing, the costs are divided into fixed, semi-variable and variable costs. Semi-variable costs are again classified into fixed and variable elements. The cost of product is ascertained by including the variable cost only.

Marginal Costing

Thus, Marginal cost is ascertained using variable costs which can be summarized as follows: The fixed costs are charged against the year’s profit i.e. these are charged in the period in which these are incurred. The closing stock is also valued according to marginal cost i.e. without including fixed overheads. In short, marginal costing is a technique of ascertaining marginal cost and break-even/ cost-volume profit analysis. Marginal costing is also known as Direct costing, variable costing and contributory costing. Now, let us understand the detailed meaning of the three very backbones of marginal costing.

Variable Cost: Variable cost is that part of cost which varies with the level of output. The variable cost per unit does not change, but the total variable cost increases/decreases in proportion to the level of output.Fixed Cost: Fixed cost is that part of cost which remains fixed irrespective of the level of output. The total fixed remains constant, but the fixed cost per unit keeps on changing with change in level of activity because the same amount will be divided over different number of units. Also, remember that

Total Cost = Fixed Cost + Variable Cost

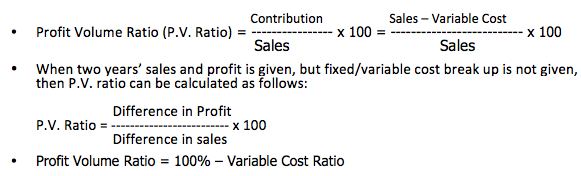

Contribution: Contribution is the excess of sales over the variable cost. It is called as ‘contribution’ because it contributes towards recovery of the fixed cost and profit. So, these are simple formulae to derive contribution:Contribution = Sale – Variable CostContribution = Sales x P.V. RatioContribution = Fixed Cost + Profit

Now, another important topic is the P. V. Ratio. (Profit volume ratio)

It is a ratio of contribution as a percentage of sales. It remains fixed irrespective of the level of output. It can be also termed as contribution volume ratio. It does not get affected by change in fixed cost. However, this ratio suffers from certain limitations in practical scenarios because the assumptions of break-even analysis may not hold true. Analysis of a concept is equally important for proper and complete understanding. Let us analyze the ways in which the PV Ratio can be improved:

Increase in Selling Price.Improvement in Production Technology so as to reduce the variable cost.Reduction of variable selling and distribution costs.Buying raw materials in bulk so as to reduce the cost per unit.

This is the basic knowledge which one must possess before studying Marginal Costing. After being conceptually clear, we can solve difficult questions also.

Weighted Average Cost of Capita Transfer Pricing Definition & Transfer Pricing Methods Costing – Classification of Various Costs Methods to Determine Arm’s Length Price Practical Difficulties In Application of Arm’s Length Price Profitability Index (PI) Detailed Analysis Material Requisition